Tariffs Don't Fix Trade - Capital Flows Do

The cost of escaping a recession

In an open economy driven by global finance, the external balance is determined by capital flows, not by trade itself. Formally, the balance-of-payments identity states:

Current Account + Financial Account = 0

Current Account = − (Financial Account)

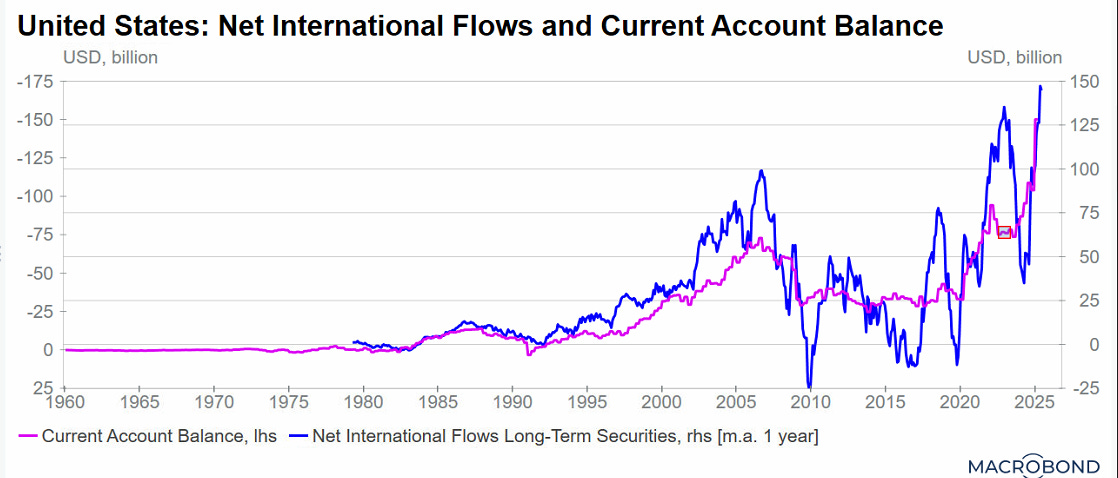

Thus, net foreign capital inflows, a financial-account surplus, require a current-account deficit. As long as investors around the world seek out U.S. assets, the United States must import more than it exports. This reverses conventional thinking: it is capital inflows that cause the trade deficit, not the other way around.

In such a system, tariffs do not reduce the external deficit directly. If imports do not contract in volume immediately, tariffs merely alter income distribution domestically. The relevant identity is:

(Sp−I) + (T−G) = (X−M)

where Sp denotes the private-sector savings (households and corporates), I denote…