What If?

What If America Loses the War

To understand what it would mean for America to “lose the war,” one must first understand the system it built after the collapse of Bretton Woods, because what is at stake is not a battlefield outcome but the architecture of global power itself, and that architecture was reconstructed in the early 1970s when the United States, having severed the dollar from gold under Richard Nixon, faced the urgent need to anchor its currency in something else, something that would preserve global demand for dollars in the absence of convertibility, and what emerged, quietly, strategically, and with extraordinary consequence, was the alignment of energy, security, and capital flows into what later came to be known as the petrodollar system.

This system was never simply about pricing oil in dollars, as is often repeated in simplified narratives, but rather about creating a closed loop in which every economy that sold energy needed dollars and every economy that needed energy needed dollars, and every economy that sold energy accumulated those dollars and needed a place to store them, and that place was the United States, whose financial markets provided depth, liquidity, and political protection, while in return the United States guaranteed something far more valuable than any monetary arrangement: it guaranteed security, of regimes, of infrastructure, and of the maritime routes through which energy flows, and this implicit contract, oil for dollars, dollars for Treasuries, Treasuries for security, became the foundation of the modern global system.

The historical moment that accelerated and cemented this structure was the Yom Kippur War and the subsequent oil embargo, when energy was weaponized and the world was forced to confront the reality that control over oil meant control over the global economy, and it was in the aftermath of that shock, amid inflation, scarcity, and geopolitical realignment, that the United States and key oil producers, particularly Saudi Arabia, moved into a strategic arrangement that was not born out of alignment of interests but out of necessity and balance of power, embedding the dollar at the center of energy trade while reinforcing the security guarantees that made such an arrangement credible.

The sequence of events that followed only reinforces how tightly interwoven power, finance, and geopolitics were in shaping this system, because in March 1975 King Faisal—who was not aligned in a simple or friendly manner with the United States but operated within a far more complex and often tense geopolitical framework—was assassinated, and within weeks, in April 1975, the Lebanese civil war erupted, transforming one of the most important financial and commercial hubs of the region into a fragmented battlefield, effectively removing Beirut from its role as a regional center of capital and trade, and while history rarely presents itself as a neat chain of causality, it is difficult to ignore how these events consolidated the shift of financial gravity toward a system anchored in oil revenues, dollar recycling, and U.S. financial markets, as if the old Levantine commercial order had to give way to the new petrodollar order; there are, indeed, no coincidences in history.

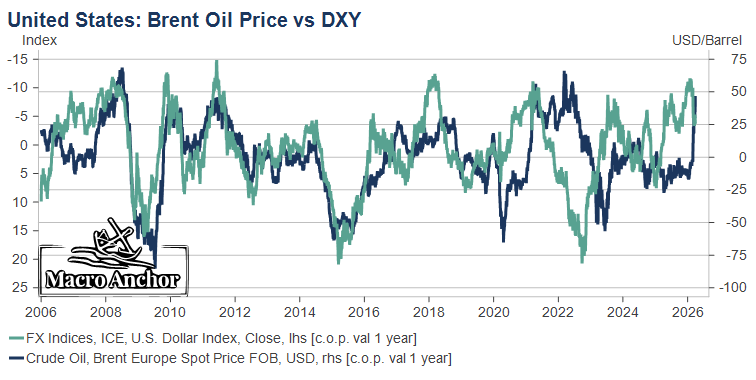

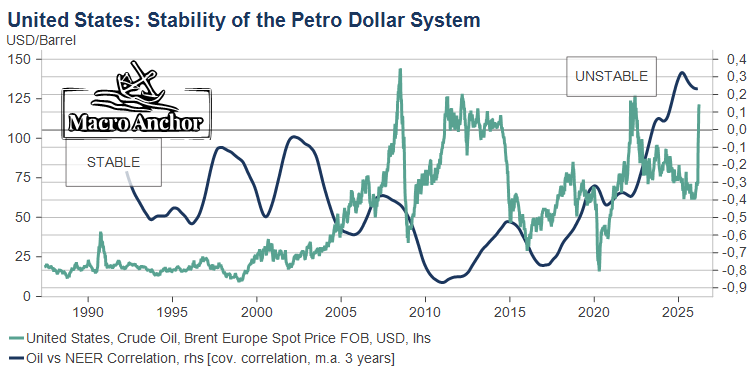

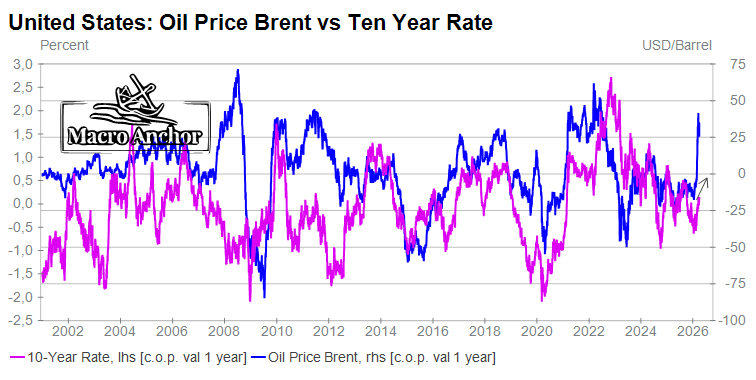

From that point onward, the system functioned with remarkable efficiency, because it created its own internal demand: every economy that needed energy needed dollars, every economy that sold energy accumulated dollars, and those dollars flowed back into U.S. assets, financing deficits that would have been unsustainable under any other arrangement, while at the same time stabilizing global markets through a mechanism that, for decades, manifested itself in the inverse relationship between the dollar and oil prices, a negative correlation that acted as a kind of pressure valve, since a stronger dollar tended to weigh on commodity prices by tightening global financial conditions, while a weaker dollar tended to support them by easing those conditions, thereby smoothing the shocks that would otherwise have destabilized the system.

Yet this relationship, like the system itself, was not immutable, and in recent years it has begun to fracture, with episodes in which both the dollar and oil rise together, creating a far more destabilizing environment for the global economy, particularly for importing countries that face the dual burden of higher energy costs and tighter financial conditions, and this shift is not merely a market anomaly but a signal that the underlying structure, the very architecture that linked energy, currency, and capital, is under strain.

This is where the question of “losing the war” takes on its real meaning, because the petrodollar system rests on three pillars, security guarantees, dollar-based energy pricing, and the recycling of surpluses into U.S. assets, and it is the first of these, security, that is now being tested, since the credibility of the entire arrangement depends on the United States’ ability to protect not only the producers but the flows themselves, to secure the Gulf, to guarantee the safety of chokepoints, and to ensure that oil moves without disruption, and if that guarantee weakens, the consequences do not unfold slowly but begin immediately to alter behavior at the level that matters most: the balance sheet.

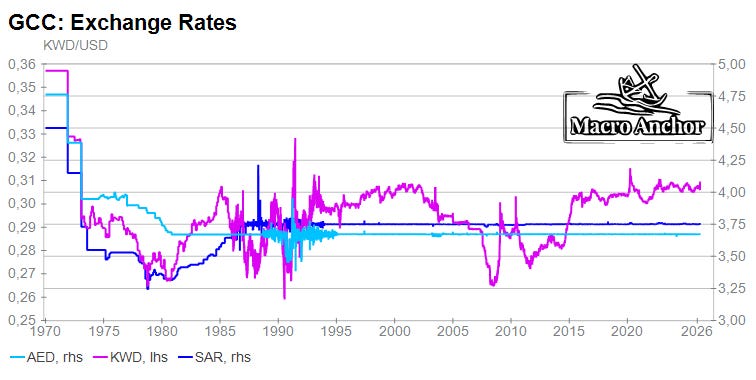

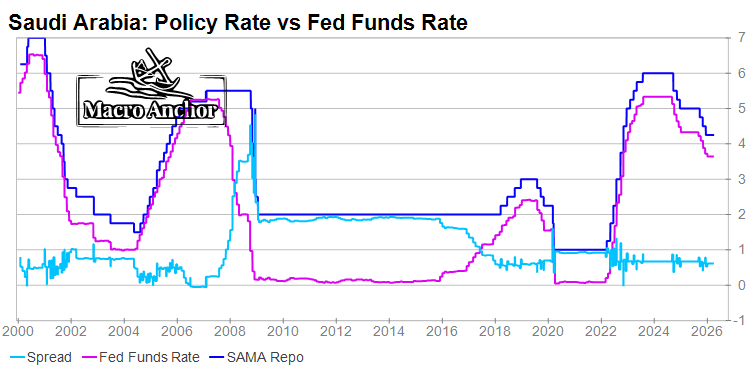

Oil does not cease to be traded in dollars overnight, nor do reserves suddenly vanish, but the assumptions that underpin those choices begin to erode. The first place this erosion becomes visible is in the exchange rate regimes of the Gulf states, whose currency pegs to the dollar, formally consolidated in 1983, central to the system, because they anchor domestic monetary conditions to the United States, enforce reserve accumulation in dollar assets, and ensure the continuity of the recycling loop, and yet these pegs are only sustainable under conditions of stability, stable revenues, stable capital flows, and above all, stable security, and when those conditions deteriorate, the cost of defending the peg rises until it collides with domestic economic needs, at which point the choice becomes unavoidable: maintain the peg and sacrifice flexibility, or abandon the peg and redefine the system.

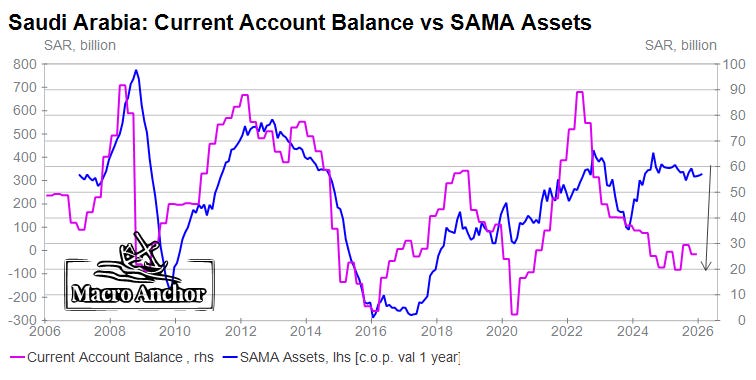

If that break occurs, it will not be gradual, and its significance will extend far beyond the currency itself, because it will signal that the strategic alignment at the heart of the petrodollar system has fractured, that reserves will begin to diversify, that oil revenues will no longer automatically return to U.S. markets, and that the relationship between oil and the dollar will be fundamentally altered, since higher oil prices will no longer guarantee stronger dollar inflows but may instead accelerate the shift away from dollar concentration, turning what was once a reinforcing mechanism into a dilutive one.

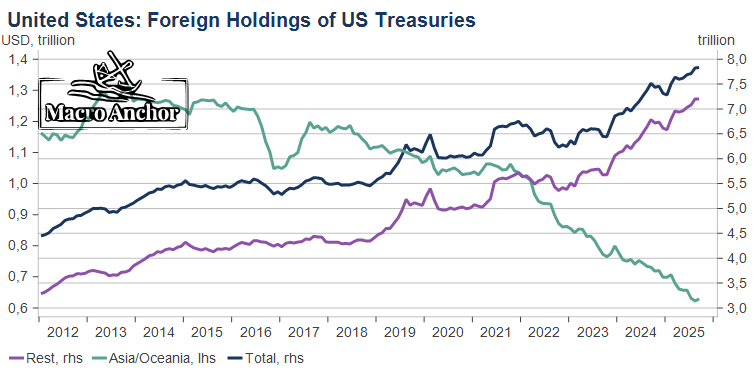

At that point, the consequences propagate through the system, reaching the U.S. Treasury market, where foreign central banks and sovereign entities have long played a structural role as buyers of American debt, and where even a marginal reduction in demand, less accumulation, slower recycling, greater diversification, can have profound effects, because the issue is not what is sold but what is no longer bought, and in a world of persistent U.S. deficits, the absence of that marginal buyer forces an adjustment, either through higher yields that attract capital at a cost, or through increased reliance on domestic absorption, with all the implications that entails for monetary policy, financial conditions, and economic stability, meaning a total monetization of the deficits.

This is the point at which the analogy with the post-Vietnam War era becomes more than rhetorical, because the 1970s were defined by a loss of monetary control, by oil shocks, by inflation, and by the search for a new anchor after the collapse of the old system, and while the United States ultimately reasserted its position through the construction of the petrodollar order, the transition itself was volatile and costly, and today the scale of the system is far larger, the levels of debt far higher, and the dependence on continuous capital inflows far more pronounced, suggesting that any comparable transition would be even more disruptive.

To say that America might “lose the war” is therefore not to predict defeat in a conventional sense but to describe a shift in the underlying mechanics of power, a shift in which the United States moves from being the issuer of the global system to being a participant within a more fragmented and less predictable order, where the ability to finance deficits, to stabilize markets, and to project influence is constrained not by military capability but by the willingness of others to continue operating within the system it created.

The petrodollar system was never permanent; it was a structure built on alignment, necessity, and power, and its endurance depended on the credibility of each of its pillars, so that when security weakens, pegs come under pressure, reserves begin to diversify, and capital flows adjust, the system does not collapse in a single moment but begins to unwind, gradually at first and then more decisively, until the loop that once sustained it is no longer intact.

And that is the real meaning of the question, because the loss is not marked by a flag coming down or a treaty being signed, but by a change in behavior—in how oil is priced, in how reserves are held, in how capital flows—and once those behaviors change, the system that defined the past half century gives way to something else, something not yet fully formed, but already visible in the fractures that are beginning to appear.

Happy Easter,

May Peace reign all over the World.

Regards,

Andre Chelhot, CFA

Editor,

The Macro Anchor

what do you make of the argument by E.M. Burlinggame, Tom Luongo (Youtube) and others that this administration is attempting to re-assert the Hamiltonian, Henry Carey American system (see the Sec of Commerce speech at Davos; i.e. divorce from the old British Empire completely and adopt ARC (America, Russia, China) power politics.

The US Empire is funded by a structural trade deficit. How can this be sustainable without eventually ruining the currency? ("exorbitant privilege" or "deficits without tears"). The answer was found around 1968 by a working group around Volcker and Kissinger. The US control a resource (then oil) that every industrial country needs. The US team up with the major producer (then Saudi Arabia) and make sure oil is available only for USD. Every other industrial country now needs USD in order to purchase essential energy. In the long run, there is only one sustainable way of obtaining these USD: by running a structural trade surplus with the US. That's what we know as "globalization". It's how the empire is funded. In order to maintain this system, however, the US need to (1) adjust the USD oil price from time to time, just in order to "regulate" economic activity in the other countries and (2) keep potential competition to Saudi Arabia off the market. Re (2), you can see, for example, that Iraq regularly suffered a war when their production reached 3mm bbl/day: 1979/80 Iran-Iraq war; 1990/91 Operation Desert Storm; 2003 US attack under pretext of weapons of mass destruction; 2013/14 the rise of the Islamic State. Occasionally, further competitors have to be taken out, sanctions against Iran or Venezuela; 2012 attack on Libya,... you'll probably find further cases. So the "1999 Cheney Agenda" was about taking out the competition, in particular Iraq who were selling for EUR rather than USD. The Abdullah government of Saudi Arabia signaled around 1997 that they would consider shifting to EUR when introduced. Iraq UN 'oil for food" programme from 2000 was in EUR. KSA King Fahd had heart attacks and due to health Abdullah became regent, that was 1998. So KSA planned move to Euro was a work which started before it went online. Saddam was the first country to switch and was stopped. Iraq under the UN "oil for food programme, 1999" was the test balloon. It was a French plot to hold the oil proceeds in EUR in some escrow account at BNP Paribas. It must have been around 1997 (when China showed up in the gold market and almost blew up LBMA) that Saudis signaled to Europe that they would be interested in supporting the EUR. Last minute, BIS raised the gold ratio of EUR to 15% of reserves, just for Saudis. Euro launched 1999. Britain was divided about joining or not. Spring 2001 King Abdullah wrote to GW Bush and announced an end to their cooperation ("There comes a time when nations must part..."). US had been aiming for Iraq since before GW Bush inauguration in Jan 2001. First move of new admin was "Cheney Energy Task Force" to figure out how dangerous a EUR selling Iraq would be and how to stop them. 9/11 provided a pretext for attacking Iraq. US had been forcing inflation onto the world since the early 1970s. Saudis sold way more oil than they needed to fund their imports, and so wanted something long term stable. Europe offered gold and Euro. I am convinced that if you would let Venezuela, Iran, Iraq explore and develop peacefully, the world would have ample cheap to produce oil for many decades if not centuries. But the USD would lose its international role and the empire its funding if that were to happen. Now, after 2008 during the first Obama administration, the US must have decided that oil was becoming less and nat gas more relevant. So they decided to re-peg the USD to gas instead. If that's decided, the competitor you need to remove is no longer Iraq, Iran, but rather Russia. It seems that Obama & Biden admins have this nat gas agenda. Thus less hostile to Iran, but extremely hostile to Russia. Trump, in contrast, was a glimpse from the past with an oil focus. Not that hostile to Russia, but more so to Iran. Re MbS from Saudi Arabia, here are some observations. Obama government after 2008 must have decided to replace oil backing of USD with gas backing. Saudis must have gotten wind and needed a plan B. Summer 2014 Saudi foreign secretary Al Saud suddenly went to Moscow several times (first high level contact ever). Then Oct 2014 suddenly Russia & Saudis chaired OPEC conference together, oil price crashed. Jan 2015 Abdullah died (had long been ill, apparently government was being restructured much earlier). MbS was de facto successor. ECB quantitative easing starts March 2015 although EUR debt crisis of 2010-12 was over. Made no sense until Chris Cook told us that Saudis were shifting to EUR and ECB was simply making room for them. Then 2016 Trump gets elected, oil people, re-approaches Saudis. Gas faction (Obama, Clinton, Biden) opposes. Very plausible rumour says CIA tried to assassinate MbS, but military & Trump faction foiled the attack. Alwaleed bin Talal must have been among those who set the trap for MbS. Hence 2017 cleansing & Ryadh Ritz Carlton torture camp. MbS had "old Fahd gang" killed or silenced. Now Biden broke with Trump, continues Obama gas policy. Question is where do Saudis stand? In none of these cases (Iraq, Libya, Iran), the US had to actually take the foreign oil. It was enough to topple the other countries' infrastructure and create chaos, removing competitors from the market. The current Ukraine crisis is a case in point. Before 2014, most of Europe's gas pipelines went through Ukraine. So the US sponsored the 2014 Maidan coup d'état in order to get a hand on the valve to Europe. Germany's Merkel government countered that by building Nord Stream 2, rendering Ukraine irrelevant as a transit country. So in order to gain control of Europe's gas supply, the US began to arm Ukraine and to fund the anti-Russian extremist government there, setting Ukraine ...up to one day attack Russia. Now they managed to provoke Russia earlier, and also they managed to get the German government under control. There we are. Either them or their poodle finally blew up the pipeline, and now all nat gas for Europe arrives by sea and is paid for in USD. The US successfully conscripted Western Europe to funding their empire for a few further decades, using the old mechanism, just with nat gas instead of oil. Removing the energy supply to Europe is important for another reason. Since Nord Stream 1 (around 2007?), Russia has been shipping more and more gas to Europe, for EUR, and Russia began to accumulate EUR reserves. So Russia became to the EUR what Saudi Arabia used to be for the USD. The EUR emerged as an alternative reserve currency and enjoyed substantial commodity backing, allowing the ECB a "little but growing exorbitant privilege". The US would do anything short of global thermonuclear war in order to get rid of that competing reserve currency. Now we know they did indeed. After 9/11 it was obvious that in order to move away from the petrodollar, only a nuclear power could make the first step, and do so probably only at gun point (Russia did by ditching its dollar reserves). Et voilà.